Nothing

README.md

In seasonal: R Interface to X-13-ARIMA-SEATS

R interface to X-13ARIMA-SEATS

seasonal is an easy-to-use and full-featured R-interface to X-13ARIMA-SEATS,

the newest seasonal adjustment software developed by the United States Census

Bureau.

Installation

seasonal depends on the x13binary package to access pre-built

binaries of X-13ARIMA-SEATS on all platforms and does not require any manual

installation. To install both packages:

install.packages("seasonal")

Getting started

seas is the core function of the seasonal package. By default, seas calls

the automatic procedures of X-13ARIMA-SEATS to perform a seasonal adjustment

that works well in most circumstances:

m <- seas(AirPassengers)

For a more detailed introduction, check our article in the Journal of

Statistical Software or consider the

vignette:

vignette("seas")

Input

In seasonal, it is possible to use almost the complete syntax of

X-13ARIMA-SEATS. The X-13ARIMA-SEATS syntax uses specs and arguments, with each spec

optionally containing some arguments. These spec-argument combinations can be

added to seas by separating the spec and the argument by a dot (.). For

example, in order to set the 'variables' argument of the 'regression' spec equal

to td and ao1999.jan, the input to seas looks like this:

m <- seas(AirPassengers, regression.variables = c("td", "ao1955.jan"))

The best way to learn about the relationship between the syntax of

X-13ARIMA-SEATS and seasonal is to study the comprehensive list of examples.

Detailed information on the options can be found in the Census Bureaus'

official manual.

Output

seasonal has a flexible mechanism to read data from X-13ARIMA-SEATS. With the

series function, it is possible to import almost all output that can be

generated by X-13ARIMA-SEATS. For example, the following command returns the

forecasts of the ARIMA model as a "ts" time series:

m <- seas(AirPassengers)

series(m, "forecast.forecasts")

Graphs

There are several graphical tools to analyze a seas model. The main plot

function draws the seasonally adjusted and unadjusted series, as well as the

outliers:

m <- seas(AirPassengers, regression.aictest = c("td", "easter"))

plot(m)

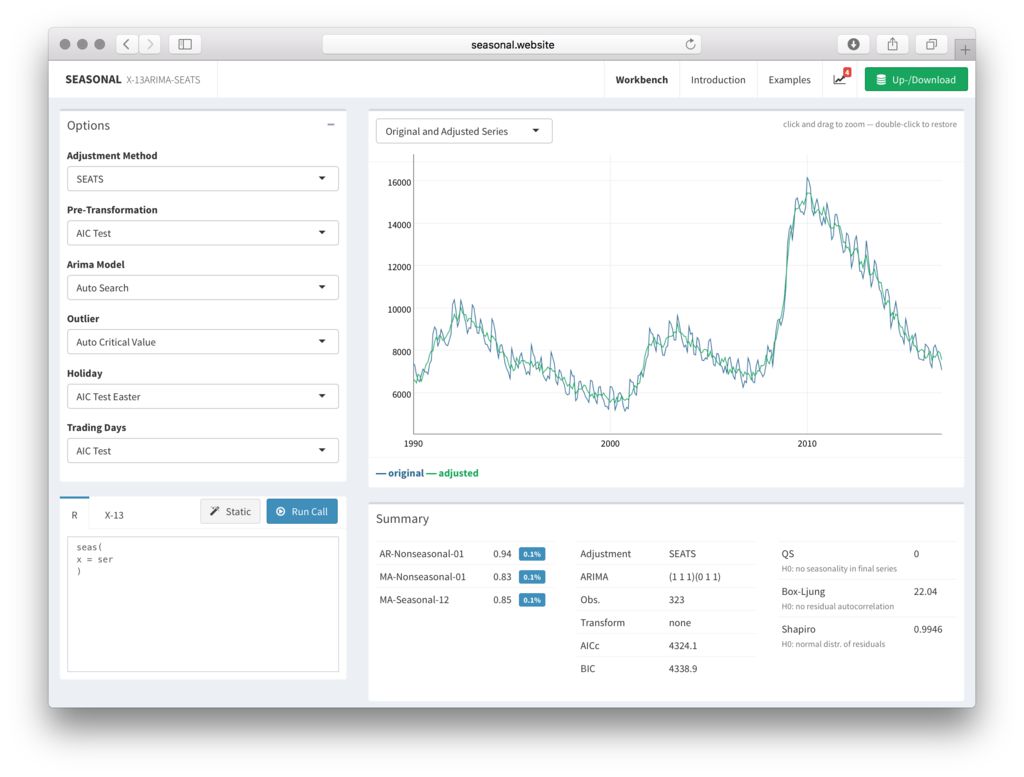

Graphical User Interface

The view function is a graphical tool for choosing a seasonal adjustment

model, using the seasonalview package, with the same

structure as the demo website of seasonal. To install

seasonalview, type:

install.packages("seasonalview")

The goal of view is to summarize all relevant options, plots and statistics

that should be usually considered. view uses a "seas" object as its main

argument:

view(m)

License

seasonal is free and open source, licensed under GPL-3. It requires the

X-13ARIMA-SEATS software by the U.S. Census Bureau, which is open source and

freely available under the terms of its own license.

To cite seasonal in publications use:

Sax C, Eddelbuettel D (2018). “Seasonal Adjustment by X-13ARIMA-SEATS

in R.” Journal of Statistical Software, 87(11), 1-17. doi:

10.18637/jss.v087.i11 (URL: https://doi.org/10.18637/jss.v087.i11).

Please report bugs and suggestions on GitHub. Thank you!

Try the seasonal package in your browser

Any scripts or data that you put into this service are public.

seasonal documentation built on Oct. 20, 2024, 1:08 a.m.

R Package Documentation

Browse R Packages

We want your feedback!

Note that we can't provide technical support on individual packages. You should contact the package authors for that.

R interface to X-13ARIMA-SEATS

![]()

seasonal is an easy-to-use and full-featured R-interface to X-13ARIMA-SEATS, the newest seasonal adjustment software developed by the United States Census Bureau.

Installation

seasonal depends on the x13binary package to access pre-built binaries of X-13ARIMA-SEATS on all platforms and does not require any manual installation. To install both packages:

install.packages("seasonal")

Getting started

seas is the core function of the seasonal package. By default, seas calls

the automatic procedures of X-13ARIMA-SEATS to perform a seasonal adjustment

that works well in most circumstances:

m <- seas(AirPassengers)

For a more detailed introduction, check our article in the Journal of Statistical Software or consider the vignette:

vignette("seas")

Input

In seasonal, it is possible to use almost the complete syntax of

X-13ARIMA-SEATS. The X-13ARIMA-SEATS syntax uses specs and arguments, with each spec

optionally containing some arguments. These spec-argument combinations can be

added to seas by separating the spec and the argument by a dot (.). For

example, in order to set the 'variables' argument of the 'regression' spec equal

to td and ao1999.jan, the input to seas looks like this:

m <- seas(AirPassengers, regression.variables = c("td", "ao1955.jan"))

The best way to learn about the relationship between the syntax of X-13ARIMA-SEATS and seasonal is to study the comprehensive list of examples. Detailed information on the options can be found in the Census Bureaus' official manual.

Output

seasonal has a flexible mechanism to read data from X-13ARIMA-SEATS. With the

series function, it is possible to import almost all output that can be

generated by X-13ARIMA-SEATS. For example, the following command returns the

forecasts of the ARIMA model as a "ts" time series:

m <- seas(AirPassengers)

series(m, "forecast.forecasts")

Graphs

There are several graphical tools to analyze a seas model. The main plot

function draws the seasonally adjusted and unadjusted series, as well as the

outliers:

m <- seas(AirPassengers, regression.aictest = c("td", "easter"))

plot(m)

Graphical User Interface

The view function is a graphical tool for choosing a seasonal adjustment

model, using the seasonalview package, with the same

structure as the demo website of seasonal. To install

seasonalview, type:

install.packages("seasonalview")

The goal of view is to summarize all relevant options, plots and statistics

that should be usually considered. view uses a "seas" object as its main

argument:

view(m)

License

seasonal is free and open source, licensed under GPL-3. It requires the X-13ARIMA-SEATS software by the U.S. Census Bureau, which is open source and freely available under the terms of its own license.

To cite seasonal in publications use:

Sax C, Eddelbuettel D (2018). “Seasonal Adjustment by X-13ARIMA-SEATS in R.” Journal of Statistical Software, 87(11), 1-17. doi: 10.18637/jss.v087.i11 (URL: https://doi.org/10.18637/jss.v087.i11).

Please report bugs and suggestions on GitHub. Thank you!

Try the seasonal package in your browser

Any scripts or data that you put into this service are public.

R Package Documentation

Browse R Packages

We want your feedback!

Note that we can't provide technical support on individual packages. You should contact the package authors for that.

Embedding an R snippet on your website

Add the following code to your website.

For more information on customizing the embed code, read Embedding Snippets.