inst/examples/BUGS/parametric-vs-nonparametric.md

In cboettig/nonparametric-bayes: Nonparametric Bayes inference for ecological models

Comparison of Nonparametric Bayesian Gaussian Process estimates to standard the Parametric Bayesian approach

Plotting and knitr options, (can generally be ignored)

require(modeest)

posterior.mode <- function(x) {

mlv(x, method="shorth")$M

}

Model and parameters

f <- Myers

p <- c(1, 2, 6)

K <- 5 # approx, a li'l' less

allee <- 1.2 # approx, a li'l' less

Various parameters defining noise dynamics, grid, and policy costs.

sigma_g <- 0.05

sigma_m <- 0.0

z_g <- function() rlnorm(1, 0, sigma_g)

z_m <- function() 1+(2*runif(1, 0, 1)-1) * sigma_m

x_grid <- seq(0, 1.5 * K, length=50)

h_grid <- x_grid

profit <- function(x,h) pmin(x, h)

delta <- 0.01

OptTime <- 50 # stationarity with unstable models is tricky thing

reward <- 0

xT <- 0

Xo <- allee+.5# observations start from

x0 <- K # simulation under policy starts from

Tobs <- 40

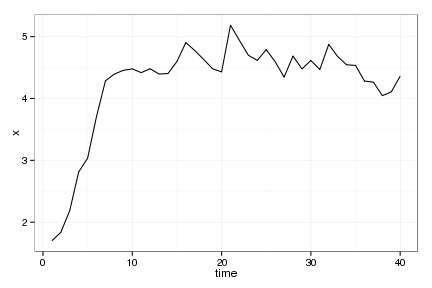

Sample Data

set.seed(1234)

#harvest <- sort(rep(seq(0, .5, length=7), 5))

x <- numeric(Tobs)

x[1] <- Xo

nz <- 1

for(t in 1:(Tobs-1))

x[t+1] = z_g() * f(x[t], h=0, p=p)

obs <- data.frame(x = c(rep(0,nz),

pmax(rep(0,Tobs-1), x[1:(Tobs-1)])),

y = c(rep(0,nz),

x[2:Tobs]))

raw_plot <- ggplot(data.frame(time = 1:Tobs, x=x), aes(time,x)) + geom_line()

raw_plot

Maximum Likelihood

set.seed(12345)

estf <- function(p){

mu <- f(obs$x,0,p)

-sum(dlnorm(obs$y, log(mu), p[4]), log=TRUE)

}

par <- c(p[1]*rlnorm(1,0,.2),

p[2]*rlnorm(1,0,.1),

p[3]*rlnorm(1,0, .1),

sigma_g * rlnorm(1,0,.3))

o <- optim(par, estf, method="L", lower=c(1e-5,1e-5,1e-5,1e-5))

f_alt <- f

p_alt <- c(as.numeric(o$par[1]), as.numeric(o$par[2]), as.numeric(o$par[3]))

sigma_g_alt <- as.numeric(o$par[4])

est <- list(f = f_alt, p = p_alt, sigma_g = sigma_g_alt, mloglik=o$value)

Mean predictions

true_means <- sapply(x_grid, f, 0, p)

est_means <- sapply(x_grid, est$f, 0, est$p)

Non-parametric Bayes

#inv gamma has mean b / (a - 1) (assuming a>1) and variance b ^ 2 / ((a - 2) * (a - 1) ^ 2) (assuming a>2)

s2.p <- c(5,5)

d.p = c(10, 1/0.1)

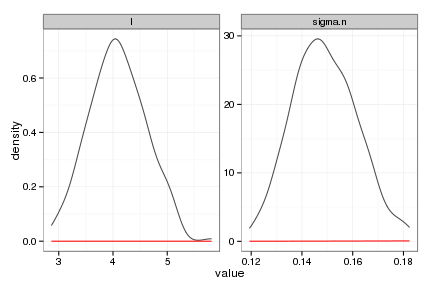

Estimate the Gaussian Process (nonparametric Bayesian fit)

gp <- gp_mcmc(obs$x, y=obs$y, n=1e5, s2.p = s2.p, d.p = d.p)

gp_dat <- gp_predict(gp, x_grid, burnin=1e4, thin=300)

Show traces and posteriors against priors

plots <- summary_gp_mcmc(gp, burnin=1e4, thin=300)

# Summarize the GP model

tgp_dat <-

data.frame( x = x_grid,

y = gp_dat$E_Ef,

ymin = gp_dat$E_Ef - 2 * sqrt(gp_dat$E_Vf),

ymax = gp_dat$E_Ef + 2 * sqrt(gp_dat$E_Vf) )

Parametric Bayesian Models

We use the JAGS Gibbs sampler, a recent open source BUGS

implementation with an R interface that works on most platforms.

We initialize the usual MCMC parameters; see ?jags for details.

All parametric Bayesian estimates use the following basic parameters for the JAGS MCMC:

y <- x

N <- length(x);

jags.data <- list("N","y")

n.chains <- 6

n.iter <- 1e6

n.burnin <- floor(10000)

n.thin <- max(1, floor(n.chains * (n.iter - n.burnin)/1000))

n.update <- 10

We will use the same priors for process and observation noise in each model,

stdQ_prior_p <- c(1e-6, 100)

stdR_prior_p <- c(1e-6, .1)

stdQ_prior <- function(x) dunif(x, stdQ_prior_p[1], stdQ_prior_p[2])

stdR_prior <- function(x) dunif(x, stdR_prior_p[1], stdR_prior_p[2])

Parametric Bayes of correct (Allen) model

We initiate the MCMC chain (init_p) using the true values of the

parameters p from the simulation. While impossible in real data, this

gives the parametric Bayesian approach the best chance at succeeding.

y is the timeseries (recall obs has the $x_t$, $x_{t+1}$ pairs)

The actual model is defined in a model.file that contains an R function

that is automatically translated into BUGS code by R2WinBUGS. The file

defines the priors and the model. We write the file from R as follows:

K_prior_p <- c(0.01, 20.0)

r0_prior_p <- c(0.01, 6.0)

theta_prior_p <- c(0.01, 20.0)

bugs.model <-

paste(sprintf(

"model{

K ~ dunif(%s, %s)

r0 ~ dunif(%s, %s)

theta ~ dunif(%s, %s)

stdQ ~ dunif(%s, %s)",

K_prior_p[1], K_prior_p[2],

r0_prior_p[1], r0_prior_p[2],

theta_prior_p[1], theta_prior_p[2],

stdQ_prior_p[1], stdQ_prior_p[2]),

"

iQ <- 1 / (stdQ * stdQ);

y[1] ~ dunif(0, 10)

for(t in 1:(N-1)){

mu[t] <- log(y[t]) + r0 * (1 - y[t]/K)* (y[t] - theta) / K

y[t+1] ~ dlnorm(mu[t], iQ)

}

}")

writeLines(bugs.model, "allen_process.bugs")

Write the priors into a list for later reference

K_prior <- function(x) dunif(x, K_prior_p[1], K_prior_p[2])

r0_prior <- function(x) dunif(x, r0_prior_p[1], r0_prior_p[2])

theta_prior <- function(x) dunif(x, theta_prior_p[1], theta_prior_p[2])

par_priors <- list(K = K_prior, deviance = function(x) 0 * x,

r0 = r0_prior, theta = theta_prior,

stdQ = stdQ_prior)

We define which parameters to keep track of, and set the initial values of

parameters in the transformed space used by the MCMC. We use logarithms

to maintain strictly positive values of parameters where appropriate.

jags.params=c("K","r0","theta","stdQ") # be sensible about the order here

jags.inits <- function(){

list("K"= 8 * rlnorm(1,0, 0.1),

"r0"= 2 * rlnorm(1,0, 0.1) ,

"theta"= 5 * rlnorm(1,0, 0.1) ,

"stdQ"= abs( 0.1 * rlnorm(1,0, 0.1)),

.RNG.name="base::Wichmann-Hill", .RNG.seed=123)

}

set.seed(1234)

# parallel refuses to take variables as arguments (e.g. n.iter = 1e5 works, but n.iter = n doesn't)

allen_jags <- do.call(jags.parallel, list(data=jags.data, inits=jags.inits,

jags.params, n.chains=n.chains,

n.iter=n.iter, n.thin=n.thin,

n.burnin=n.burnin,

model.file="allen_process.bugs"))

# Run again iteratively if we haven't met the Gelman-Rubin convergence criterion

recompile(allen_jags) # required for parallel

allen_jags <- do.call(autojags,

list(object=allen_jags, n.update=n.update,

n.iter=n.iter, n.thin = n.thin))

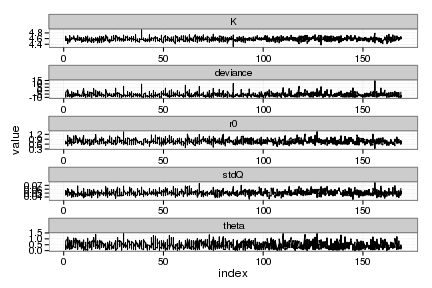

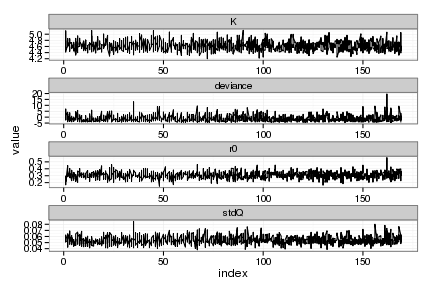

Convergence diagnostics for Allen model

R notes: this strips classes from the mcmc.list object (so that we have list of matrices; objects that reshape2::melt can handle intelligently), and then combines chains into one array. In this array each parameter is given its value at each sample from the posterior (index) for each chain.

tmp <- lapply(as.mcmc(allen_jags), as.matrix) # strip classes the hard way...

allen_posteriors <- melt(tmp, id = colnames(tmp[[1]]))

names(allen_posteriors) = c("index", "variable", "value", "chain")

ggplot(allen_posteriors) + geom_line(aes(index, value)) +

facet_wrap(~ variable, scale="free", ncol=1)

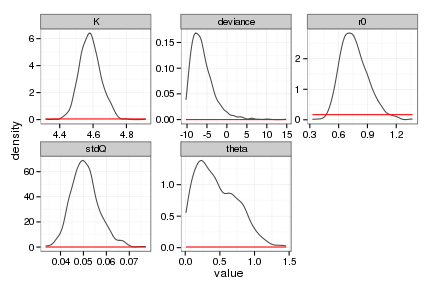

allen_priors <- ddply(allen_posteriors, "variable", function(dd){

grid <- seq(min(dd$value), max(dd$value), length = 100)

data.frame(value = grid, density = par_priors[[dd$variable[1]]](grid))

})

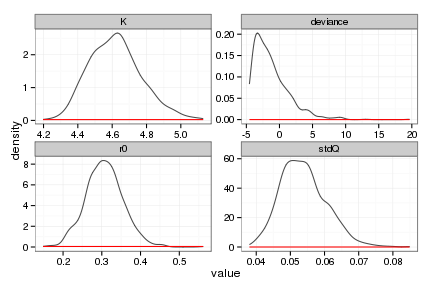

ggplot(allen_posteriors, aes(value)) +

stat_density(geom="path", position="identity", alpha=0.7) +

geom_line(data=allen_priors, aes(x=value, y=density), col="red") +

facet_wrap(~ variable, scale="free", ncol=3)

Reshape the posterior parameter distribution data, transform back into original space, and calculate the mean parameters and mean function

A <- allen_posteriors

A$index <- A$index + A$chain * max(A$index) # Combine samples across chains by renumbering index

pardist <- acast(A, index ~ variable)

bayes_coef <- apply(pardist,2, posterior.mode)

bayes_pars <- unname(c(bayes_coef["r0"], bayes_coef["K"], bayes_coef["theta"])) # parameters formatted for f

allen_f <- function(x,h,p) unname(RickerAllee(x,h, unname(p[c("r0", "K", "theta")])))

allen_means <- sapply(x_grid, f, 0, bayes_pars)

bayes_pars

[1] 0.7082 4.5647 0.2558

head(pardist)

K deviance r0 stdQ theta

170 4.531 -8.534 0.6867 0.04473 0.3832

171 4.516 1.335 0.6471 0.05928 1.0216

172 4.574 -8.576 0.8532 0.04983 0.7196

173 4.614 -6.873 0.5302 0.04611 0.1390

174 4.628 -5.580 0.7331 0.04024 0.5064

175 4.503 -7.443 0.7341 0.04474 0.2369

Parametric Bayes based on the structurally wrong model (Ricker)

K_prior_p <- c(0.01, 40.0)

r0_prior_p <- c(0.01, 20.0)

bugs.model <-

paste(sprintf(

"model{

K ~ dunif(%s, %s)

r0 ~ dunif(%s, %s)

stdQ ~ dunif(%s, %s)",

K_prior_p[1], K_prior_p[2],

r0_prior_p[1], r0_prior_p[2],

stdQ_prior_p[1], stdQ_prior_p[2]),

"

iQ <- 1 / (stdQ * stdQ);

y[1] ~ dunif(0, 10)

for(t in 1:(N-1)){

mu[t] <- log(y[t]) + r0 * (1 - y[t]/K)

y[t+1] ~ dlnorm(mu[t], iQ)

}

}")

writeLines(bugs.model, "ricker_process.bugs")

Compute prior curves

K_prior <- function(x) dunif(x, K_prior_p[1], K_prior_p[2])

r0_prior <- function(x) dunif(x, r0_prior_p[1], r0_prior_p[2])

par_priors <- list(K = K_prior, deviance = function(x) 0 * x,

r0 = r0_prior, stdQ = stdQ_prior)

We define which parameters to keep track of, and set the initial values of

parameters in the transformed space used by the MCMC.

jags.params=c("K","r0", "stdQ")

jags.inits <- function(){

list("K"=10 * rlnorm(1,0,.5),

"r0"= rlnorm(1,0,.5),

"stdQ"=sqrt(0.05) * rlnorm(1,0,.5),

.RNG.name="base::Wichmann-Hill", .RNG.seed=123)

}

set.seed(12345)

ricker_jags <- do.call(jags.parallel,

list(data=jags.data, inits=jags.inits,

jags.params, n.chains=n.chains,

n.iter=n.iter, n.thin=n.thin, n.burnin=n.burnin,

model.file="ricker_process.bugs"))

recompile(ricker_jags)

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

ricker_jags <- do.call(autojags,

list(object=ricker_jags, n.update=n.update,

n.iter=n.iter, n.thin = n.thin,

progress.bar="none"))

Convergence diagnostics for parametric bayes Ricker model

tmp <- lapply(as.mcmc(ricker_jags), as.matrix) # strip classes the hard way...

ricker_posteriors <- melt(tmp, id = colnames(tmp[[1]]))

names(ricker_posteriors) = c("index", "variable", "value", "chain")

ggplot(ricker_posteriors) + geom_line(aes(index, value)) +

facet_wrap(~ variable, scale="free", ncol=1)

ricker_priors <- ddply(ricker_posteriors, "variable", function(dd){

grid <- seq(min(dd$value), max(dd$value), length = 100)

data.frame(value = grid, density = par_priors[[dd$variable[1]]](grid))

})

# plot posterior distributions

ggplot(ricker_posteriors, aes(value)) +

stat_density(geom="path", position="identity", alpha=0.7) +

geom_line(data=ricker_priors, aes(x=value, y=density), col="red") +

facet_wrap(~ variable, scale="free", ncol=2)

Reshape posteriors data, transform back, calculate mode and corresponding function.

A <- ricker_posteriors

A$index <- A$index + A$chain * max(A$index) # Combine samples across chains by renumbering index

ricker_pardist <- acast(A, index ~ variable)

bayes_coef <- apply(ricker_pardist,2, posterior.mode)

ricker_bayes_pars <- unname(c(bayes_coef["r0"], bayes_coef["K"]))

ricker_f <- function(x,h,p){

sapply(x, function(x){

x <- pmax(0, x-h)

pmax(0, x * exp(p["r0"] * (1 - x / p["K"] )) )

})

}

ricker_means <- sapply(x_grid, Ricker, 0, ricker_bayes_pars[c(1,2)])

head(ricker_pardist)

K deviance r0 stdQ

170 4.796 -2.4558 0.2928 0.05125

171 4.604 4.2228 0.4464 0.06022

172 4.579 -3.6943 0.2798 0.05368

173 4.727 0.8348 0.2275 0.06162

174 4.686 0.1420 0.2346 0.04685

175 4.361 -0.5967 0.2783 0.05220

ricker_bayes_pars

[1] 0.302 4.597

Myers Parametric Bayes

r0_prior_p <- c(.0001, 10.0)

theta_prior_p <- c(.0001, 10.0)

K_prior_p <- c(.0001, 40.0)

bugs.model <-

paste(sprintf(

"model{

r0 ~ dunif(%s, %s)

theta ~ dunif(%s, %s)

K ~ dunif(%s, %s)

stdQ ~ dunif(%s, %s)",

r0_prior_p[1], r0_prior_p[2],

theta_prior_p[1], theta_prior_p[2],

K_prior_p[1], K_prior_p[2],

stdQ_prior_p[1], stdQ_prior_p[2]),

"

iQ <- 1 / (stdQ * stdQ);

y[1] ~ dunif(0, 10)

for(t in 1:(N-1)){

mu[t] <- log(r0) + theta * log(y[t]) - log(1 + pow(abs(y[t]), theta) / K)

y[t+1] ~ dlnorm(mu[t], iQ)

}

}")

writeLines(bugs.model, "myers_process.bugs")

K_prior <- function(x) dunif(x, K_prior_p[1], K_prior_p[2])

r_prior <- function(x) dunif(x, r0_prior_p[1], r0_prior_p[2])

theta_prior <- function(x) dunif(x, theta_prior_p[1], theta_prior_p[2])

par_priors <- list( deviance = function(x) 0 * x, K = K_prior,

r0 = r_prior, theta = theta_prior,

stdQ = stdQ_prior)

jags.params=c("r0", "theta", "K", "stdQ")

jags.inits <- function(){

list("r0"= rlnorm(1,0,.1),

"K"= 6 * rlnorm(1,0,.1),

"theta" = 2 * rlnorm(1,0,.1),

"stdQ"= 0.1 * rlnorm(1,0,.1),

.RNG.name="base::Wichmann-Hill", .RNG.seed=123)

}

set.seed(12345)

myers_jags <- do.call(jags.parallel,

list(data=jags.data, inits=jags.inits,

jags.params, n.chains=n.chains,

n.iter=n.iter, n.thin=n.thin,

n.burnin=n.burnin,

model.file="myers_process.bugs"))

recompile(myers_jags)

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

myers_jags <- do.call(autojags,

list(myers_jags, n.update=n.update,

n.iter=n.iter, n.thin = n.thin,

progress.bar="none"))

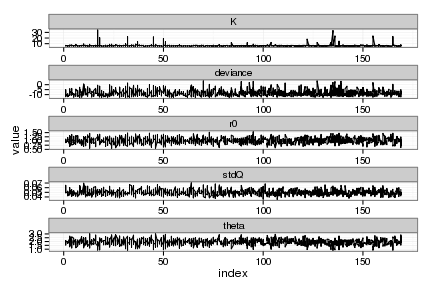

Convergence diagnostics for parametric bayes

tmp <- lapply(as.mcmc(myers_jags), as.matrix) # strip classes

myers_posteriors <- melt(tmp, id = colnames(tmp[[1]]))

names(myers_posteriors) = c("index", "variable", "value", "chain")

ggplot(myers_posteriors) + geom_line(aes(index, value)) +

facet_wrap(~ variable, scale="free", ncol=1)

par_prior_curves <- ddply(myers_posteriors, "variable", function(dd){

grid <- seq(min(dd$value), max(dd$value), length = 100)

data.frame(value = grid, density = par_priors[[dd$variable[1]]](grid))

})

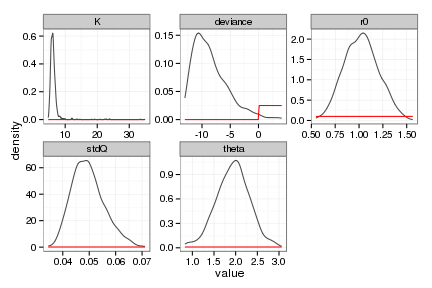

ggplot(myers_posteriors, aes(value)) +

stat_density(geom="path", position="identity", alpha=0.7) +

geom_line(data=par_prior_curves, aes(x=value, y=density), col="red") +

facet_wrap(~ variable, scale="free", ncol=3)

A <- myers_posteriors

A$index <- A$index + A$chain * max(A$index) # Combine samples across chains by renumbering index

myers_pardist <- acast(A, index ~ variable)

bayes_coef <- apply(myers_pardist,2, posterior.mode) # much better estimates

myers_bayes_pars <- unname(c(bayes_coef[2], bayes_coef[3], bayes_coef[1]))

myers_means <- sapply(x_grid, Myer_harvest, 0, myers_bayes_pars)

myers_f <- function(x,h,p) Myer_harvest(x, h, p[c("r0", "theta", "K")])

head(myers_pardist)

K deviance r0 stdQ theta

170 5.444 -11.950 1.0954 0.04771 1.879

171 5.791 -11.106 1.0380 0.04859 1.939

172 6.866 -10.293 0.7794 0.04780 2.390

173 6.454 -8.193 0.9440 0.05598 1.942

174 6.509 -10.105 0.8041 0.04375 2.444

175 7.039 -9.427 0.7927 0.04561 2.297

myers_bayes_pars

[1] -10.158 1.001 5.891

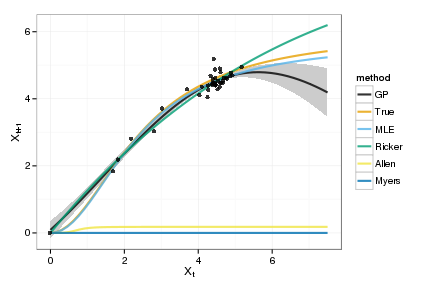

Phase-space diagram of the expected dynamics

models <- data.frame(x=x_grid,

GP=tgp_dat$y,

True=true_means,

MLE=est_means,

Ricker=ricker_means,

Allen = allen_means,

Myers = myers_means)

models <- melt(models, id="x")

# some labels

names(models) <- c("x", "method", "value")

# labels for the colorkey too

model_names = c("GP", "True", "MLE", "Ricker", "Allen", "Myers")

colorkey=cbPalette

names(colorkey) = model_names

plot_gp <- ggplot(tgp_dat) + geom_ribbon(aes(x,y,ymin=ymin,ymax=ymax), fill="gray80") +

geom_line(data=models, aes(x, value, col=method), lwd=1, alpha=0.8) +

geom_point(data=obs, aes(x,y), alpha=0.8) +

xlab(expression(X[t])) + ylab(expression(X[t+1])) +

scale_colour_manual(values=cbPalette)

print(plot_gp)

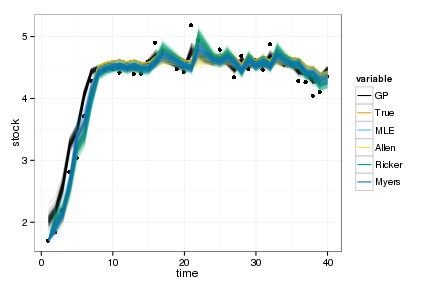

Goodness of fit

This shows only the mean predictions. For the Bayesian cases, we can instead loop over the posteriors of the parameters (or samples from the GP posterior) to get the distribution of such curves in each case.

require(MASS)

step_ahead <- function(x, f, p){

h = 0

x_predict <- sapply(x, f, h, p)

n <- length(x_predict) - 1

y <- c(x[1], x_predict[1:n])

y

}

step_ahead_posteriors <- function(x){

gp_f_at_obs <- gp_predict(gp, x, burnin=1e4, thin=300)

df_post <- melt(lapply(sample(100),

function(i){

data.frame(time = 1:length(x), stock = x,

GP = mvrnorm(1, gp_f_at_obs$Ef_posterior[,i], gp_f_at_obs$Cf_posterior[[i]]),

True = step_ahead(x,f,p),

MLE = step_ahead(x,f,est$p),

Allen = step_ahead(x, allen_f, pardist[i,]),

Ricker = step_ahead(x, ricker_f, ricker_pardist[i,]),

Myers = step_ahead(x, myers_f, myers_pardist[i,]))

}), id=c("time", "stock"))

}

df_post <- step_ahead_posteriors(x)

ggplot(df_post) + geom_point(aes(time, stock)) +

geom_line(aes(time, value, col=variable, group=interaction(L1,variable)), alpha=.1) +

scale_colour_manual(values=colorkey, guide = guide_legend(override.aes = list(alpha = 1)))

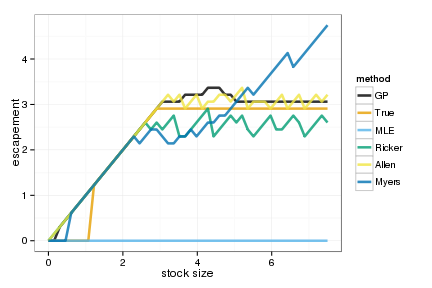

Optimal policies by value iteration

Compute the optimal policy under each model using stochastic dynamic programming. We begin with the policy based on the GP model,

MaxT = 1000

# uses expected values from GP, instead of integrating over posterior

#matrices_gp <- gp_transition_matrix(gp_dat$E_Ef, gp_dat$E_Vf, x_grid, h_grid)

# Integrate over posteriors

matrices_gp <- gp_transition_matrix(gp_dat$Ef_posterior, gp_dat$Vf_posterior, x_grid, h_grid)

# Solve the SDP using the GP-derived transition matrix

opt_gp <- value_iteration(matrices_gp, x_grid, h_grid, MaxT, xT, profit, delta, reward)

Determine the optimal policy based on the allen and MLE models

matrices_true <- f_transition_matrix(f, p, x_grid, h_grid, sigma_g)

opt_true <- value_iteration(matrices_true, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

matrices_estimated <- f_transition_matrix(est$f, est$p, x_grid, h_grid, est$sigma_g)

opt_estimated <- value_iteration(matrices_estimated, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Determine the optimal policy based on Bayesian Allen model

matrices_allen <- parameter_uncertainty_SDP(allen_f, x_grid, h_grid, pardist, 4)

opt_allen <- value_iteration(matrices_allen, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Bayesian Ricker

matrices_ricker <- parameter_uncertainty_SDP(ricker_f, x_grid, h_grid, as.matrix(ricker_pardist), 3)

opt_ricker <- value_iteration(matrices_ricker, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Bayesian Myers model

matrices_myers <- parameter_uncertainty_SDP(myers_f, x_grid, h_grid, as.matrix(myers_pardist), 4)

myers_alt <- value_iteration(matrices_myers, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Assemble the data

OPT = data.frame(GP = opt_gp$D, True = opt_true$D, MLE = opt_estimated$D, Ricker = opt_ricker$D, Allen = opt_allen$D, Myers = myers_alt$D)

colorkey=cbPalette

names(colorkey) = names(OPT)

Graph of the optimal policies

policies <- melt(data.frame(stock=x_grid, sapply(OPT, function(x) x_grid[x])), id="stock")

names(policies) <- c("stock", "method", "value")

ggplot(policies, aes(stock, stock - value, color=method)) +

geom_line(lwd=1.2, alpha=0.8) + xlab("stock size") + ylab("escapement") +

scale_colour_manual(values=colorkey)

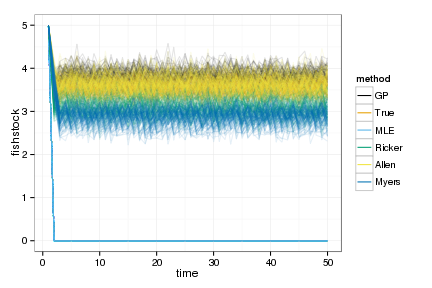

Simulate 100 realizations managed under each of the policies

sims <- lapply(OPT, function(D){

set.seed(1)

lapply(1:100, function(i)

ForwardSimulate(f, p, x_grid, h_grid, x0, D, z_g, profit=profit, OptTime=OptTime)

)

})

dat <- melt(sims, id=names(sims[[1]][[1]]))

dt <- data.table(dat)

setnames(dt, c("L1", "L2"), c("method", "reps"))

# Legend in original ordering please, not alphabetical:

dt$method = factor(dt$method, ordered=TRUE, levels=names(OPT))

ggplot(dt) +

geom_line(aes(time, fishstock, group=interaction(reps,method), color=method), alpha=.1) +

scale_colour_manual(values=colorkey, guide = guide_legend(override.aes = list(alpha = 1)))

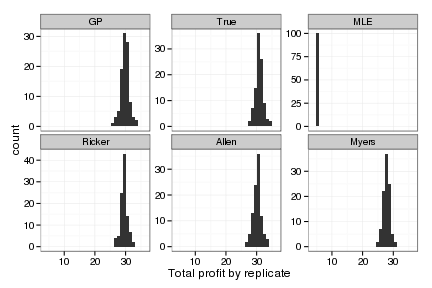

Profit <- dt[, sum(profit), by=c("reps", "method")]

Profit[, mean(V1), by="method"]

method V1

1: GP 30.06

2: True 31.14

3: MLE 5.00

4: Ricker 29.82

5: Allen 30.53

6: Myers 27.93

ggplot(Profit, aes(V1)) + geom_histogram() +

facet_wrap(~method, scales = "free_y") + guides(legend.position = "none") + xlab("Total profit by replicate")

allen_deviance <- posterior.mode(pardist[,'deviance'])

ricker_deviance <- posterior.mode(ricker_pardist[,'deviance'])

myers_deviance <- posterior.mode(myers_pardist[,'deviance'])

true_deviance <- 2*estf(c(p, sigma_g))

mle_deviance <- 2*estf(c(est$p, est$sigma_g))

c(allen = allen_deviance, ricker=ricker_deviance, myers=myers_deviance, true=true_deviance, mle=mle_deviance)

allen ricker myers true mle

-7.529 -2.893 -10.158 -106.638 -16204.252

cboettig/nonparametric-bayes documentation built on May 13, 2019, 2:09 p.m.

R Package Documentation

Browse R Packages

We want your feedback!

Note that we can't provide technical support on individual packages. You should contact the package authors for that.

Comparison of Nonparametric Bayesian Gaussian Process estimates to standard the Parametric Bayesian approach

Plotting and knitr options, (can generally be ignored)

require(modeest)

posterior.mode <- function(x) {

mlv(x, method="shorth")$M

}

Model and parameters

f <- Myers

p <- c(1, 2, 6)

K <- 5 # approx, a li'l' less

allee <- 1.2 # approx, a li'l' less

Various parameters defining noise dynamics, grid, and policy costs.

sigma_g <- 0.05

sigma_m <- 0.0

z_g <- function() rlnorm(1, 0, sigma_g)

z_m <- function() 1+(2*runif(1, 0, 1)-1) * sigma_m

x_grid <- seq(0, 1.5 * K, length=50)

h_grid <- x_grid

profit <- function(x,h) pmin(x, h)

delta <- 0.01

OptTime <- 50 # stationarity with unstable models is tricky thing

reward <- 0

xT <- 0

Xo <- allee+.5# observations start from

x0 <- K # simulation under policy starts from

Tobs <- 40

Sample Data

set.seed(1234)

#harvest <- sort(rep(seq(0, .5, length=7), 5))

x <- numeric(Tobs)

x[1] <- Xo

nz <- 1

for(t in 1:(Tobs-1))

x[t+1] = z_g() * f(x[t], h=0, p=p)

obs <- data.frame(x = c(rep(0,nz),

pmax(rep(0,Tobs-1), x[1:(Tobs-1)])),

y = c(rep(0,nz),

x[2:Tobs]))

raw_plot <- ggplot(data.frame(time = 1:Tobs, x=x), aes(time,x)) + geom_line()

raw_plot

Maximum Likelihood

set.seed(12345)

estf <- function(p){

mu <- f(obs$x,0,p)

-sum(dlnorm(obs$y, log(mu), p[4]), log=TRUE)

}

par <- c(p[1]*rlnorm(1,0,.2),

p[2]*rlnorm(1,0,.1),

p[3]*rlnorm(1,0, .1),

sigma_g * rlnorm(1,0,.3))

o <- optim(par, estf, method="L", lower=c(1e-5,1e-5,1e-5,1e-5))

f_alt <- f

p_alt <- c(as.numeric(o$par[1]), as.numeric(o$par[2]), as.numeric(o$par[3]))

sigma_g_alt <- as.numeric(o$par[4])

est <- list(f = f_alt, p = p_alt, sigma_g = sigma_g_alt, mloglik=o$value)

Mean predictions

true_means <- sapply(x_grid, f, 0, p)

est_means <- sapply(x_grid, est$f, 0, est$p)

Non-parametric Bayes

#inv gamma has mean b / (a - 1) (assuming a>1) and variance b ^ 2 / ((a - 2) * (a - 1) ^ 2) (assuming a>2)

s2.p <- c(5,5)

d.p = c(10, 1/0.1)

Estimate the Gaussian Process (nonparametric Bayesian fit)

gp <- gp_mcmc(obs$x, y=obs$y, n=1e5, s2.p = s2.p, d.p = d.p)

gp_dat <- gp_predict(gp, x_grid, burnin=1e4, thin=300)

Show traces and posteriors against priors

plots <- summary_gp_mcmc(gp, burnin=1e4, thin=300)

# Summarize the GP model

tgp_dat <-

data.frame( x = x_grid,

y = gp_dat$E_Ef,

ymin = gp_dat$E_Ef - 2 * sqrt(gp_dat$E_Vf),

ymax = gp_dat$E_Ef + 2 * sqrt(gp_dat$E_Vf) )

Parametric Bayesian Models

We use the JAGS Gibbs sampler, a recent open source BUGS

implementation with an R interface that works on most platforms.

We initialize the usual MCMC parameters; see ?jags for details.

All parametric Bayesian estimates use the following basic parameters for the JAGS MCMC:

y <- x

N <- length(x);

jags.data <- list("N","y")

n.chains <- 6

n.iter <- 1e6

n.burnin <- floor(10000)

n.thin <- max(1, floor(n.chains * (n.iter - n.burnin)/1000))

n.update <- 10

We will use the same priors for process and observation noise in each model,

stdQ_prior_p <- c(1e-6, 100)

stdR_prior_p <- c(1e-6, .1)

stdQ_prior <- function(x) dunif(x, stdQ_prior_p[1], stdQ_prior_p[2])

stdR_prior <- function(x) dunif(x, stdR_prior_p[1], stdR_prior_p[2])

Parametric Bayes of correct (Allen) model

We initiate the MCMC chain (init_p) using the true values of the

parameters p from the simulation. While impossible in real data, this

gives the parametric Bayesian approach the best chance at succeeding.

y is the timeseries (recall obs has the $x_t$, $x_{t+1}$ pairs)

The actual model is defined in a model.file that contains an R function

that is automatically translated into BUGS code by R2WinBUGS. The file

defines the priors and the model. We write the file from R as follows:

K_prior_p <- c(0.01, 20.0)

r0_prior_p <- c(0.01, 6.0)

theta_prior_p <- c(0.01, 20.0)

bugs.model <-

paste(sprintf(

"model{

K ~ dunif(%s, %s)

r0 ~ dunif(%s, %s)

theta ~ dunif(%s, %s)

stdQ ~ dunif(%s, %s)",

K_prior_p[1], K_prior_p[2],

r0_prior_p[1], r0_prior_p[2],

theta_prior_p[1], theta_prior_p[2],

stdQ_prior_p[1], stdQ_prior_p[2]),

"

iQ <- 1 / (stdQ * stdQ);

y[1] ~ dunif(0, 10)

for(t in 1:(N-1)){

mu[t] <- log(y[t]) + r0 * (1 - y[t]/K)* (y[t] - theta) / K

y[t+1] ~ dlnorm(mu[t], iQ)

}

}")

writeLines(bugs.model, "allen_process.bugs")

Write the priors into a list for later reference

K_prior <- function(x) dunif(x, K_prior_p[1], K_prior_p[2])

r0_prior <- function(x) dunif(x, r0_prior_p[1], r0_prior_p[2])

theta_prior <- function(x) dunif(x, theta_prior_p[1], theta_prior_p[2])

par_priors <- list(K = K_prior, deviance = function(x) 0 * x,

r0 = r0_prior, theta = theta_prior,

stdQ = stdQ_prior)

We define which parameters to keep track of, and set the initial values of parameters in the transformed space used by the MCMC. We use logarithms to maintain strictly positive values of parameters where appropriate.

jags.params=c("K","r0","theta","stdQ") # be sensible about the order here

jags.inits <- function(){

list("K"= 8 * rlnorm(1,0, 0.1),

"r0"= 2 * rlnorm(1,0, 0.1) ,

"theta"= 5 * rlnorm(1,0, 0.1) ,

"stdQ"= abs( 0.1 * rlnorm(1,0, 0.1)),

.RNG.name="base::Wichmann-Hill", .RNG.seed=123)

}

set.seed(1234)

# parallel refuses to take variables as arguments (e.g. n.iter = 1e5 works, but n.iter = n doesn't)

allen_jags <- do.call(jags.parallel, list(data=jags.data, inits=jags.inits,

jags.params, n.chains=n.chains,

n.iter=n.iter, n.thin=n.thin,

n.burnin=n.burnin,

model.file="allen_process.bugs"))

# Run again iteratively if we haven't met the Gelman-Rubin convergence criterion

recompile(allen_jags) # required for parallel

allen_jags <- do.call(autojags,

list(object=allen_jags, n.update=n.update,

n.iter=n.iter, n.thin = n.thin))

Convergence diagnostics for Allen model

R notes: this strips classes from the mcmc.list object (so that we have list of matrices; objects that reshape2::melt can handle intelligently), and then combines chains into one array. In this array each parameter is given its value at each sample from the posterior (index) for each chain.

tmp <- lapply(as.mcmc(allen_jags), as.matrix) # strip classes the hard way...

allen_posteriors <- melt(tmp, id = colnames(tmp[[1]]))

names(allen_posteriors) = c("index", "variable", "value", "chain")

ggplot(allen_posteriors) + geom_line(aes(index, value)) +

facet_wrap(~ variable, scale="free", ncol=1)

allen_priors <- ddply(allen_posteriors, "variable", function(dd){

grid <- seq(min(dd$value), max(dd$value), length = 100)

data.frame(value = grid, density = par_priors[[dd$variable[1]]](grid))

})

ggplot(allen_posteriors, aes(value)) +

stat_density(geom="path", position="identity", alpha=0.7) +

geom_line(data=allen_priors, aes(x=value, y=density), col="red") +

facet_wrap(~ variable, scale="free", ncol=3)

Reshape the posterior parameter distribution data, transform back into original space, and calculate the mean parameters and mean function

A <- allen_posteriors

A$index <- A$index + A$chain * max(A$index) # Combine samples across chains by renumbering index

pardist <- acast(A, index ~ variable)

bayes_coef <- apply(pardist,2, posterior.mode)

bayes_pars <- unname(c(bayes_coef["r0"], bayes_coef["K"], bayes_coef["theta"])) # parameters formatted for f

allen_f <- function(x,h,p) unname(RickerAllee(x,h, unname(p[c("r0", "K", "theta")])))

allen_means <- sapply(x_grid, f, 0, bayes_pars)

bayes_pars

[1] 0.7082 4.5647 0.2558

head(pardist)

K deviance r0 stdQ theta

170 4.531 -8.534 0.6867 0.04473 0.3832

171 4.516 1.335 0.6471 0.05928 1.0216

172 4.574 -8.576 0.8532 0.04983 0.7196

173 4.614 -6.873 0.5302 0.04611 0.1390

174 4.628 -5.580 0.7331 0.04024 0.5064

175 4.503 -7.443 0.7341 0.04474 0.2369

Parametric Bayes based on the structurally wrong model (Ricker)

K_prior_p <- c(0.01, 40.0)

r0_prior_p <- c(0.01, 20.0)

bugs.model <-

paste(sprintf(

"model{

K ~ dunif(%s, %s)

r0 ~ dunif(%s, %s)

stdQ ~ dunif(%s, %s)",

K_prior_p[1], K_prior_p[2],

r0_prior_p[1], r0_prior_p[2],

stdQ_prior_p[1], stdQ_prior_p[2]),

"

iQ <- 1 / (stdQ * stdQ);

y[1] ~ dunif(0, 10)

for(t in 1:(N-1)){

mu[t] <- log(y[t]) + r0 * (1 - y[t]/K)

y[t+1] ~ dlnorm(mu[t], iQ)

}

}")

writeLines(bugs.model, "ricker_process.bugs")

Compute prior curves

K_prior <- function(x) dunif(x, K_prior_p[1], K_prior_p[2])

r0_prior <- function(x) dunif(x, r0_prior_p[1], r0_prior_p[2])

par_priors <- list(K = K_prior, deviance = function(x) 0 * x,

r0 = r0_prior, stdQ = stdQ_prior)

We define which parameters to keep track of, and set the initial values of parameters in the transformed space used by the MCMC.

jags.params=c("K","r0", "stdQ")

jags.inits <- function(){

list("K"=10 * rlnorm(1,0,.5),

"r0"= rlnorm(1,0,.5),

"stdQ"=sqrt(0.05) * rlnorm(1,0,.5),

.RNG.name="base::Wichmann-Hill", .RNG.seed=123)

}

set.seed(12345)

ricker_jags <- do.call(jags.parallel,

list(data=jags.data, inits=jags.inits,

jags.params, n.chains=n.chains,

n.iter=n.iter, n.thin=n.thin, n.burnin=n.burnin,

model.file="ricker_process.bugs"))

recompile(ricker_jags)

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 249

Initializing model

ricker_jags <- do.call(autojags,

list(object=ricker_jags, n.update=n.update,

n.iter=n.iter, n.thin = n.thin,

progress.bar="none"))

Convergence diagnostics for parametric bayes Ricker model

tmp <- lapply(as.mcmc(ricker_jags), as.matrix) # strip classes the hard way...

ricker_posteriors <- melt(tmp, id = colnames(tmp[[1]]))

names(ricker_posteriors) = c("index", "variable", "value", "chain")

ggplot(ricker_posteriors) + geom_line(aes(index, value)) +

facet_wrap(~ variable, scale="free", ncol=1)

ricker_priors <- ddply(ricker_posteriors, "variable", function(dd){

grid <- seq(min(dd$value), max(dd$value), length = 100)

data.frame(value = grid, density = par_priors[[dd$variable[1]]](grid))

})

# plot posterior distributions

ggplot(ricker_posteriors, aes(value)) +

stat_density(geom="path", position="identity", alpha=0.7) +

geom_line(data=ricker_priors, aes(x=value, y=density), col="red") +

facet_wrap(~ variable, scale="free", ncol=2)

Reshape posteriors data, transform back, calculate mode and corresponding function.

A <- ricker_posteriors

A$index <- A$index + A$chain * max(A$index) # Combine samples across chains by renumbering index

ricker_pardist <- acast(A, index ~ variable)

bayes_coef <- apply(ricker_pardist,2, posterior.mode)

ricker_bayes_pars <- unname(c(bayes_coef["r0"], bayes_coef["K"]))

ricker_f <- function(x,h,p){

sapply(x, function(x){

x <- pmax(0, x-h)

pmax(0, x * exp(p["r0"] * (1 - x / p["K"] )) )

})

}

ricker_means <- sapply(x_grid, Ricker, 0, ricker_bayes_pars[c(1,2)])

head(ricker_pardist)

K deviance r0 stdQ

170 4.796 -2.4558 0.2928 0.05125

171 4.604 4.2228 0.4464 0.06022

172 4.579 -3.6943 0.2798 0.05368

173 4.727 0.8348 0.2275 0.06162

174 4.686 0.1420 0.2346 0.04685

175 4.361 -0.5967 0.2783 0.05220

ricker_bayes_pars

[1] 0.302 4.597

Myers Parametric Bayes

r0_prior_p <- c(.0001, 10.0)

theta_prior_p <- c(.0001, 10.0)

K_prior_p <- c(.0001, 40.0)

bugs.model <-

paste(sprintf(

"model{

r0 ~ dunif(%s, %s)

theta ~ dunif(%s, %s)

K ~ dunif(%s, %s)

stdQ ~ dunif(%s, %s)",

r0_prior_p[1], r0_prior_p[2],

theta_prior_p[1], theta_prior_p[2],

K_prior_p[1], K_prior_p[2],

stdQ_prior_p[1], stdQ_prior_p[2]),

"

iQ <- 1 / (stdQ * stdQ);

y[1] ~ dunif(0, 10)

for(t in 1:(N-1)){

mu[t] <- log(r0) + theta * log(y[t]) - log(1 + pow(abs(y[t]), theta) / K)

y[t+1] ~ dlnorm(mu[t], iQ)

}

}")

writeLines(bugs.model, "myers_process.bugs")

K_prior <- function(x) dunif(x, K_prior_p[1], K_prior_p[2])

r_prior <- function(x) dunif(x, r0_prior_p[1], r0_prior_p[2])

theta_prior <- function(x) dunif(x, theta_prior_p[1], theta_prior_p[2])

par_priors <- list( deviance = function(x) 0 * x, K = K_prior,

r0 = r_prior, theta = theta_prior,

stdQ = stdQ_prior)

jags.params=c("r0", "theta", "K", "stdQ")

jags.inits <- function(){

list("r0"= rlnorm(1,0,.1),

"K"= 6 * rlnorm(1,0,.1),

"theta" = 2 * rlnorm(1,0,.1),

"stdQ"= 0.1 * rlnorm(1,0,.1),

.RNG.name="base::Wichmann-Hill", .RNG.seed=123)

}

set.seed(12345)

myers_jags <- do.call(jags.parallel,

list(data=jags.data, inits=jags.inits,

jags.params, n.chains=n.chains,

n.iter=n.iter, n.thin=n.thin,

n.burnin=n.burnin,

model.file="myers_process.bugs"))

recompile(myers_jags)

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

Compiling model graph

Resolving undeclared variables

Allocating nodes

Graph Size: 406

Initializing model

myers_jags <- do.call(autojags,

list(myers_jags, n.update=n.update,

n.iter=n.iter, n.thin = n.thin,

progress.bar="none"))

Convergence diagnostics for parametric bayes

tmp <- lapply(as.mcmc(myers_jags), as.matrix) # strip classes

myers_posteriors <- melt(tmp, id = colnames(tmp[[1]]))

names(myers_posteriors) = c("index", "variable", "value", "chain")

ggplot(myers_posteriors) + geom_line(aes(index, value)) +

facet_wrap(~ variable, scale="free", ncol=1)

par_prior_curves <- ddply(myers_posteriors, "variable", function(dd){

grid <- seq(min(dd$value), max(dd$value), length = 100)

data.frame(value = grid, density = par_priors[[dd$variable[1]]](grid))

})

ggplot(myers_posteriors, aes(value)) +

stat_density(geom="path", position="identity", alpha=0.7) +

geom_line(data=par_prior_curves, aes(x=value, y=density), col="red") +

facet_wrap(~ variable, scale="free", ncol=3)

A <- myers_posteriors

A$index <- A$index + A$chain * max(A$index) # Combine samples across chains by renumbering index

myers_pardist <- acast(A, index ~ variable)

bayes_coef <- apply(myers_pardist,2, posterior.mode) # much better estimates

myers_bayes_pars <- unname(c(bayes_coef[2], bayes_coef[3], bayes_coef[1]))

myers_means <- sapply(x_grid, Myer_harvest, 0, myers_bayes_pars)

myers_f <- function(x,h,p) Myer_harvest(x, h, p[c("r0", "theta", "K")])

head(myers_pardist)

K deviance r0 stdQ theta

170 5.444 -11.950 1.0954 0.04771 1.879

171 5.791 -11.106 1.0380 0.04859 1.939

172 6.866 -10.293 0.7794 0.04780 2.390

173 6.454 -8.193 0.9440 0.05598 1.942

174 6.509 -10.105 0.8041 0.04375 2.444

175 7.039 -9.427 0.7927 0.04561 2.297

myers_bayes_pars

[1] -10.158 1.001 5.891

Phase-space diagram of the expected dynamics

models <- data.frame(x=x_grid,

GP=tgp_dat$y,

True=true_means,

MLE=est_means,

Ricker=ricker_means,

Allen = allen_means,

Myers = myers_means)

models <- melt(models, id="x")

# some labels

names(models) <- c("x", "method", "value")

# labels for the colorkey too

model_names = c("GP", "True", "MLE", "Ricker", "Allen", "Myers")

colorkey=cbPalette

names(colorkey) = model_names

plot_gp <- ggplot(tgp_dat) + geom_ribbon(aes(x,y,ymin=ymin,ymax=ymax), fill="gray80") +

geom_line(data=models, aes(x, value, col=method), lwd=1, alpha=0.8) +

geom_point(data=obs, aes(x,y), alpha=0.8) +

xlab(expression(X[t])) + ylab(expression(X[t+1])) +

scale_colour_manual(values=cbPalette)

print(plot_gp)

Goodness of fit

This shows only the mean predictions. For the Bayesian cases, we can instead loop over the posteriors of the parameters (or samples from the GP posterior) to get the distribution of such curves in each case.

require(MASS)

step_ahead <- function(x, f, p){

h = 0

x_predict <- sapply(x, f, h, p)

n <- length(x_predict) - 1

y <- c(x[1], x_predict[1:n])

y

}

step_ahead_posteriors <- function(x){

gp_f_at_obs <- gp_predict(gp, x, burnin=1e4, thin=300)

df_post <- melt(lapply(sample(100),

function(i){

data.frame(time = 1:length(x), stock = x,

GP = mvrnorm(1, gp_f_at_obs$Ef_posterior[,i], gp_f_at_obs$Cf_posterior[[i]]),

True = step_ahead(x,f,p),

MLE = step_ahead(x,f,est$p),

Allen = step_ahead(x, allen_f, pardist[i,]),

Ricker = step_ahead(x, ricker_f, ricker_pardist[i,]),

Myers = step_ahead(x, myers_f, myers_pardist[i,]))

}), id=c("time", "stock"))

}

df_post <- step_ahead_posteriors(x)

ggplot(df_post) + geom_point(aes(time, stock)) +

geom_line(aes(time, value, col=variable, group=interaction(L1,variable)), alpha=.1) +

scale_colour_manual(values=colorkey, guide = guide_legend(override.aes = list(alpha = 1)))

Optimal policies by value iteration

Compute the optimal policy under each model using stochastic dynamic programming. We begin with the policy based on the GP model,

MaxT = 1000

# uses expected values from GP, instead of integrating over posterior

#matrices_gp <- gp_transition_matrix(gp_dat$E_Ef, gp_dat$E_Vf, x_grid, h_grid)

# Integrate over posteriors

matrices_gp <- gp_transition_matrix(gp_dat$Ef_posterior, gp_dat$Vf_posterior, x_grid, h_grid)

# Solve the SDP using the GP-derived transition matrix

opt_gp <- value_iteration(matrices_gp, x_grid, h_grid, MaxT, xT, profit, delta, reward)

Determine the optimal policy based on the allen and MLE models

matrices_true <- f_transition_matrix(f, p, x_grid, h_grid, sigma_g)

opt_true <- value_iteration(matrices_true, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

matrices_estimated <- f_transition_matrix(est$f, est$p, x_grid, h_grid, est$sigma_g)

opt_estimated <- value_iteration(matrices_estimated, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Determine the optimal policy based on Bayesian Allen model

matrices_allen <- parameter_uncertainty_SDP(allen_f, x_grid, h_grid, pardist, 4)

opt_allen <- value_iteration(matrices_allen, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Bayesian Ricker

matrices_ricker <- parameter_uncertainty_SDP(ricker_f, x_grid, h_grid, as.matrix(ricker_pardist), 3)

opt_ricker <- value_iteration(matrices_ricker, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Bayesian Myers model

matrices_myers <- parameter_uncertainty_SDP(myers_f, x_grid, h_grid, as.matrix(myers_pardist), 4)

myers_alt <- value_iteration(matrices_myers, x_grid, h_grid, OptTime=MaxT, xT, profit, delta=delta)

Assemble the data

OPT = data.frame(GP = opt_gp$D, True = opt_true$D, MLE = opt_estimated$D, Ricker = opt_ricker$D, Allen = opt_allen$D, Myers = myers_alt$D)

colorkey=cbPalette

names(colorkey) = names(OPT)

Graph of the optimal policies

policies <- melt(data.frame(stock=x_grid, sapply(OPT, function(x) x_grid[x])), id="stock")

names(policies) <- c("stock", "method", "value")

ggplot(policies, aes(stock, stock - value, color=method)) +

geom_line(lwd=1.2, alpha=0.8) + xlab("stock size") + ylab("escapement") +

scale_colour_manual(values=colorkey)

Simulate 100 realizations managed under each of the policies

sims <- lapply(OPT, function(D){

set.seed(1)

lapply(1:100, function(i)

ForwardSimulate(f, p, x_grid, h_grid, x0, D, z_g, profit=profit, OptTime=OptTime)

)

})

dat <- melt(sims, id=names(sims[[1]][[1]]))

dt <- data.table(dat)

setnames(dt, c("L1", "L2"), c("method", "reps"))

# Legend in original ordering please, not alphabetical:

dt$method = factor(dt$method, ordered=TRUE, levels=names(OPT))

ggplot(dt) +

geom_line(aes(time, fishstock, group=interaction(reps,method), color=method), alpha=.1) +

scale_colour_manual(values=colorkey, guide = guide_legend(override.aes = list(alpha = 1)))

Profit <- dt[, sum(profit), by=c("reps", "method")]

Profit[, mean(V1), by="method"]

method V1

1: GP 30.06

2: True 31.14

3: MLE 5.00

4: Ricker 29.82

5: Allen 30.53

6: Myers 27.93

ggplot(Profit, aes(V1)) + geom_histogram() +

facet_wrap(~method, scales = "free_y") + guides(legend.position = "none") + xlab("Total profit by replicate")

allen_deviance <- posterior.mode(pardist[,'deviance'])

ricker_deviance <- posterior.mode(ricker_pardist[,'deviance'])

myers_deviance <- posterior.mode(myers_pardist[,'deviance'])

true_deviance <- 2*estf(c(p, sigma_g))

mle_deviance <- 2*estf(c(est$p, est$sigma_g))

c(allen = allen_deviance, ricker=ricker_deviance, myers=myers_deviance, true=true_deviance, mle=mle_deviance)

allen ricker myers true mle

-7.529 -2.893 -10.158 -106.638 -16204.252

R Package Documentation

Browse R Packages

We want your feedback!

Note that we can't provide technical support on individual packages. You should contact the package authors for that.

Embedding an R snippet on your website

Add the following code to your website.

For more information on customizing the embed code, read Embedding Snippets.